Buyer Beware – Group RESPs and Scholarship Trust Plans

May 02, 2024

Group RESPs and Scholarship Trust Plans should not be mistaken for a traditional education savings plan. Great care should be taken when you are investigating your education plan options.

Group Registered Education Savings Plans, which are a type of Registered Education Savings Plan (RESP) that is managed as a Scholarship Trust Plan (STP), have emerged as a popular option for families seeking to secure their children’s educational future by saving for their post-secondary education in this vehicle. However, delving deeper into their operational mechanisms reveals a landscape filled with nuances and potential pitfalls that warrant careful consideration.

Central to the appeal of RESPs are the tax-deferred earnings and government grants they offer, with the latter represented by the Canada Education Savings Grant (CESG), which matches 20% of the initial $2,500 contributed annually, up to a lifetime limit of $7,200 per child. This incentive underscores Canada's commitment to fostering a culture of education savings. Conceptually, RESPs operate through three primary components: personal contributions, the aforementioned government grants, and the growth of investments. However, beneath this overarching framework lie distinct variations in plan structures, each carrying its own set of advantages and limitations.

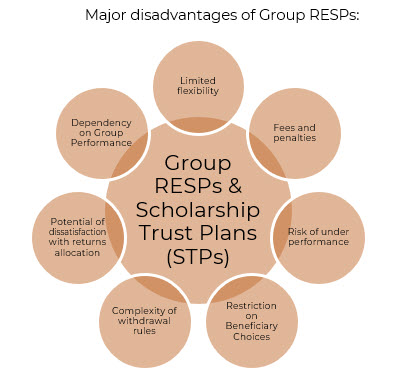

Of the three types, Individual RESPs, Family RESPs, and Group RESPs, the latter presents a more rigid and less-transparent alternative. Group RESPs pool contributions from multiple participants under the supervision of the plan provider, thereby relinquishing individual control over investment decisions. Notably, these pooled funds typically find their way into fixed-income investments, limiting the potential for substantial growth.

Group RESPs entail a distinct fee structure characterized by enrollment fees often deducted from initial contributions, uncompetitive investment fees, and rigid contribution schedules. Failure to adhere to these predetermined payment plans may jeopardize the plan’s viability, with options for altering or halting contributions proving scarce. Furthermore, the redemption process for Group RESPs is encumbered by predefined schedules and conditions, with the outcome contingent on factors beyond the contributor’s control, such as investment returns and the number of qualifying beneficiaries.

Of particular concern is the predetermined redemption schedule, which severely restricts the options available to contributors should a beneficiary choose not to pursue further education. In such instances, Group RESPs typically only return the net contributions, subtracting enrollment and management fees, while withholding government grants and accrued investment growth. This inherent inflexibility exposes contributors to significant financial losses and underscores the importance of understanding the terms and conditions before committing to such plans.

Families must conduct thorough research and carefully evaluate their options to ensure that their hard-earned savings are managed in a manner aligned with their educational aspirations for their children.