More People Qualify for The Disability Tax Credit Than You Think

Aug 14, 2024

Over the years, we have come across many clients who were unaware that they, or their loved ones, might qualify for the disability tax credit (DTC). The disability tax credit is a worthwhile consideration that can result in thousands of dollars of saved income tax.

The disability tax credit allows an individual who either has a condition, or the family member they support, to reduce the amount of income tax paid. The tax credit varies by province, but if you are a resident of BC, it could equate to roughly $1,900 in income tax savings per year for an adult, or approximately $3,000 of tax savings per year for a minor. The child disability tax credit can be applied for by either parent who is taking primary care of the child with the impairment. In addition, if you or your child were eligible for the tax credit in past years but did not claim it, you can retroactively apply, going back up to 10 years.

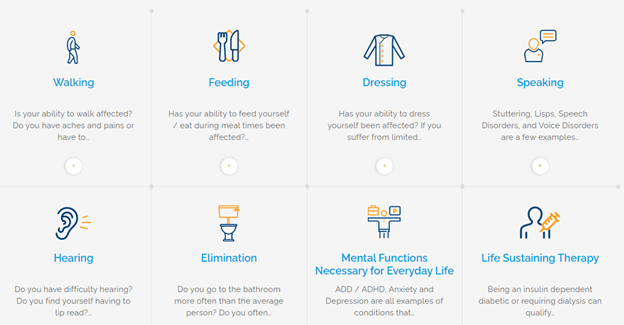

Eligibility is based on how the person is affected on a daily basis (it does not have to be a permanent or aged-related condition). Conditions that can qualify can be grouped into the following categories:

Source: True North Disability Services

Below is a list of many conditions that qualify but please note that many other conditions may be eligible as well. For example, if you have a child with asthma or celiac disease who is impacted on a regular basis, your child could qualify for the disability tax credit. A discussion with your medical practitioner can help you determine whether you or a family member might qualify.

Source: Disability Credit Canada

The process of applying for the DTC involves submitting a Disability Tax Credit Certificate (T2201) which can be found on the Government of Canada website. A medical practitioner (either a medical doctor or a specialist) must certify the application.

Getting approved for the Disability Tax Credit is a prerequisite for opening a Registered Disability Savings Plan (RDSP). This is a long-term savings plan that allows contributions to grow tax-deferred, and to potentially receive government grants and bonds to enhance your savings (if the RDSP is set up prior to age 50).

Your RGF Financial Advisor can help adjust your financial plan to incorporate the potential benefits of the disability tax credit.

Why do we plan?

Knowing where you are translates into knowing where you're going, and we hope to provide every client with the trust and confidence to navigate through the waters of their financial lives.

Learn More